One of the most common questions we’re asked by our clients is "where’s the next Thailand?"

In the intervening years, it’s been interesting to see the insurance industry take a more proactive approach to flood risk management. They’re now beginning to ask questions like "where am I exposed to flood?", "how much (re/insurance) cover do I need?", "what's the biggest loss I could expect from my portfolio?" and "which areas will be affected simultaneously?"

But, with the perennial issue of aggregate insurance exposure data and without available maps and models, this has proved challenging.

To aid our clients, we’ve developed a global coverage of flood maps. And, in 2016, we began looking more closely at probabilistic flood risk in Vietnam.

We recently released the industry's first Vietnam river and surface water flood probabilistic model, meaning our clients can be among the first to fully quantify and capture their exposure to flood risk in the region. The model highlights probable event losses, loss hotspots and loss accumulations due to correlated exposures.

We’ve taken a look at some of the most important questions regarding Vietnam flood below.

What's the annual impact of flooding in Vietnam?

What's the annual impact of flooding in Vietnam?

Annually, the average number of people exposed to flood in Vietnam is 2.1 million with the annual average loss to flood estimate at $575 million USD.

Pictured right: Regions of Vietnam, with the three most frequently flooded highlighted in orange

Are the new industrial sites in Vietnam exposed to flood?

Over 60% of industrial parks are within the 1-in-50-year flood extent. We examined the locations of the major industrial parks which, buoyed by foreign investment, have grown rapidly in recent years and made attractive locations for multi-national corporations.

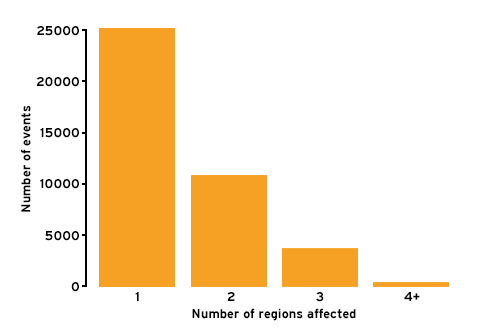

How are the events distributed in Vietnam?

How are the events distributed in Vietnam?

Of the 48,000 simulated events in our Vietnam model, most affect the Northern Midlands and Mountains, Red River Delta and North and South Central Coast regions. Events in the Red River Delta are the major driver of multiple regions being affected; this area includes a major concentration of exposure in Hanoi.

Can Hanoi and Ho Chi Minh City flood simultaneously?

Hanoi and Ho Chi Minh City are spatially independent, with no simultaneous flooding.

Interestingly, none of the events with an overall loss return period exceeding 200 years cause any loss in Ho Chi Minh City, which is in the Southeast region, despite it being a large city with substantial exposure.

What's the outlook for Vietnam's insurance industry?

What's the outlook for Vietnam's insurance industry?

Whilst the boom in industrial park development is beginning to slow, the insurance market is still growing. Recent figures published in Asia Insurance Magazine indicated that total premium revenues in Vietnam reached $3.8 billion USD in 2016 and are predicted to rise by a further 20% in 2017.

As economic losses rise and the insurance gap narrows, without considered flood risk management, insured losses seem likely to follow.

Pictured right: Exposure in Vietnam is concentrated close to the populous cities of Ho Chi Minh City and Hanoi

What do our clients think about our model?

Since the model's launch last month, we’ve received overwhelmingly positive feedback as insurers, reinsurers and brokers can further enhance their current risk management practice in Vietnam.

Among those excited to see a new Vietnam model is UIB Asia:

Vietnam is a very important market for us and we’re extremely pleased to be making use of JBA’s new Vietnam Flood model. Vietnam flood risk, like many other South East Asian countries, is a major peril and having a full probabilistic model to assess that risk is immensely helpful. We are looking forward to collaborating with JBA to enhance the services that we provide to our growing client base in Vietnam

If you're interested in understanding your exposure, cover requirements and possible losses, get in touch today for more information on our Vietnam Flood Probabilistic Model.